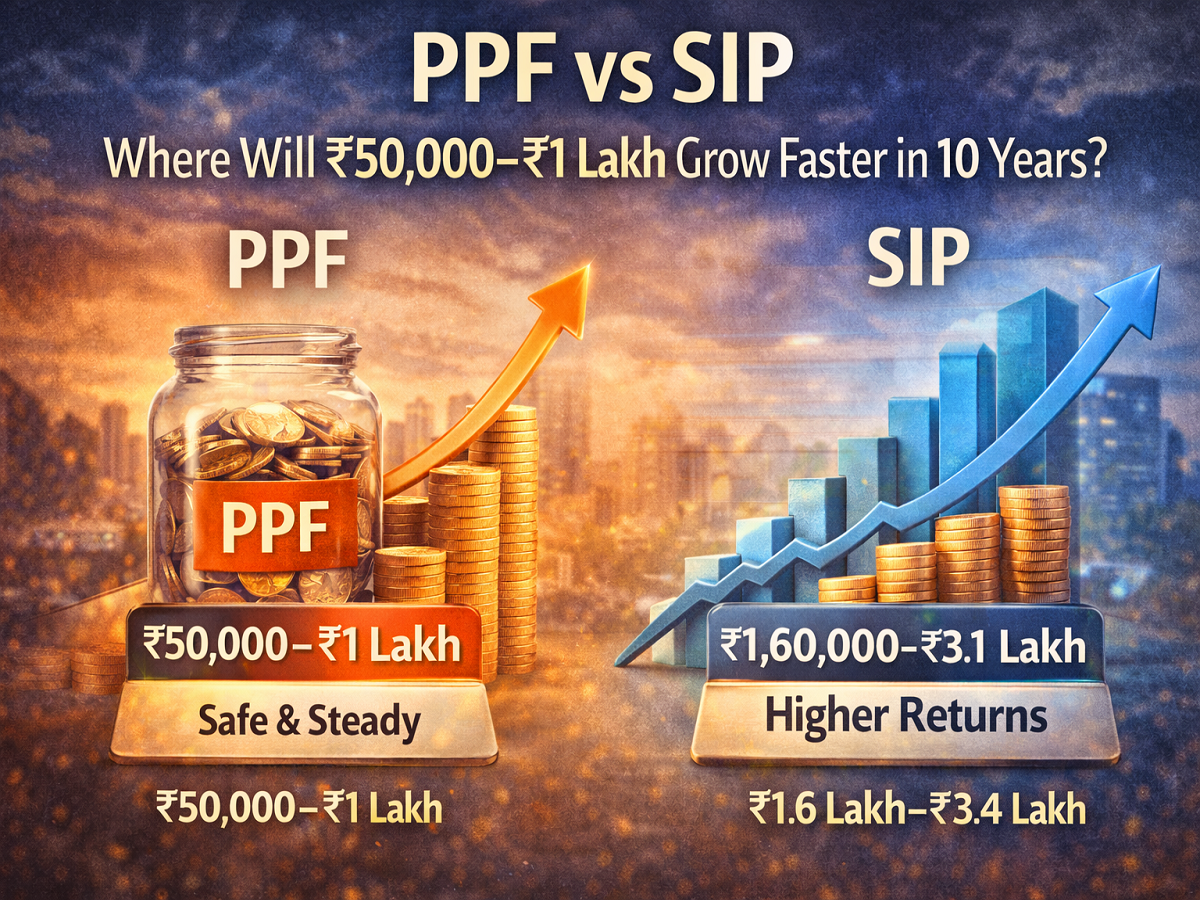

When it comes to building wealth in a disciplined way, two popular options often dominate the conversation in India—Public Provident Fund (PPF) and Systematic Investment Plan (SIP). If you’re planning to invest anywhere between ₹50,000 and ₹1 lakh for a 10-year period, choosing the right option can significantly impact your financial outcome.

But here’s the truth: there is no one-size-fits-all answer. Both PPF and SIP serve different purposes, and understanding how they work is key to making a smart investment decision.

Understanding PPF: Safety with Stability

The Public Provident Fund is a government-backed savings scheme known for its safety and guaranteed returns. It currently offers interest rates in the range of around 7–8%, which are revised periodically by the government.

Key Features of PPF:

- Completely risk-free investment

- Fixed and predictable returns

- Tax benefits under Section 80C

- Interest and maturity amount are tax-free

- Long-term lock-in period of 15 years

PPF is ideal for conservative investors who prioritize capital protection over high returns. While it may not deliver aggressive growth, it ensures steady accumulation over time.

What Is SIP and How Does It Work?

A Systematic Investment Plan is a method of investing in mutual funds, particularly equity funds. Unlike PPF, SIP is market-linked, meaning returns are not fixed.

Key Highlights of SIP:

- Potential returns of 10–15% annually (historically)

- Market-linked growth with compounding benefits

- Flexibility in investment amount and duration

- No fixed lock-in (except ELSS funds)

SIP is widely considered a powerful tool for wealth creation, especially for long-term investors willing to take moderate risk.

10-Year Investment: What Difference Can It Make?

If you invest ₹50,000 to ₹1 lakh regularly or even as a lump sum for 10 years, the difference in returns between PPF and SIP can be significant.

- PPF: Offers stable growth with predictable returns

- SIP: Can potentially generate 40–60% higher returns over the same period

For example, while PPF steadily grows your investment, SIP leverages market performance and compounding, which can accelerate wealth creation over time.

Risk vs Return: The Core Difference

The biggest difference between these two options lies in risk.

- PPF is risk-free, backed by the government

- SIP carries market risk, meaning returns can fluctuate

In bullish market conditions, SIP investments can outperform significantly. However, during market downturns, returns may be lower or even negative in the short term.

This makes SIP suitable for investors with a higher risk appetite, while PPF suits those seeking stability.

Which Option Is Right for You?

Choosing between PPF and SIP depends on your financial goals and risk tolerance.

Choose PPF if:

- You want guaranteed returns

- You prefer low-risk investments

- You are looking for tax-saving options

- You are investing for long-term financial security

Choose SIP if:

- You aim for higher returns

- You can tolerate market fluctuations

- You are investing for wealth creation

- You have a long-term investment horizon

Can You Invest in Both? Absolutely

The smartest approach, according to many financial experts, is not choosing one over the other—but combining both.

A balanced strategy can help you:

- Protect your capital through PPF

- Grow your wealth through SIP

This diversification reduces risk while improving your chances of better overall returns.

Smart Strategy for ₹50,000–₹1 Lakh Investment

If you’re planning to invest within this range, here’s a practical approach:

- Allocate a portion to PPF for safety and tax benefits

- Invest the remaining amount in SIP for growth potential

This way, you benefit from both stability and higher return opportunities.

Final Thoughts

Both Public Provident Fund and Systematic Investment Plan have their own strengths. While SIP has the potential to grow your money faster over 10 years, PPF offers unmatched security and peace of mind.

Ultimately, the best investment strategy is one that aligns with your goals, risk tolerance, and time horizon. By making informed choices and staying consistent, even a ₹50,000–₹1 lakh investment can turn into a substantial corpus over a decade.